When it comes to build a balanced cross asset portfolio of Risk Premia, one of the issues that needs to be addressed is the relative weight of each asset class

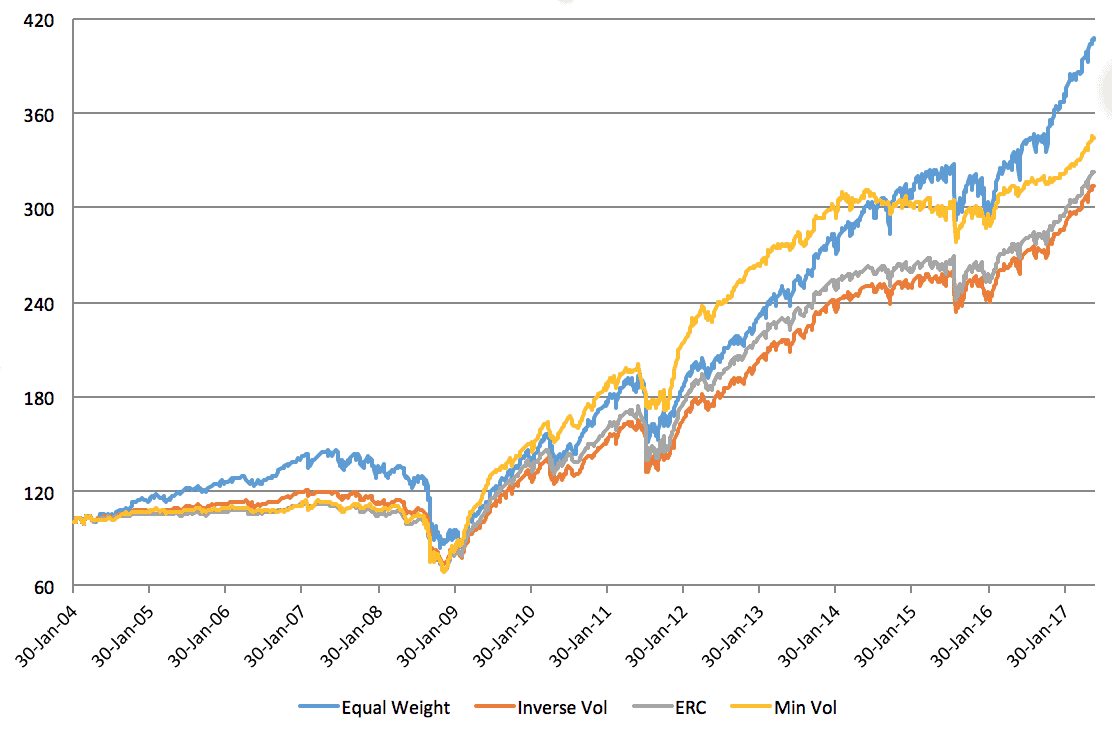

Let's consider a portfolio of 8 absolute return Risk Premia strategies, from different providers and asset classes, and having at least 3 years of track record.

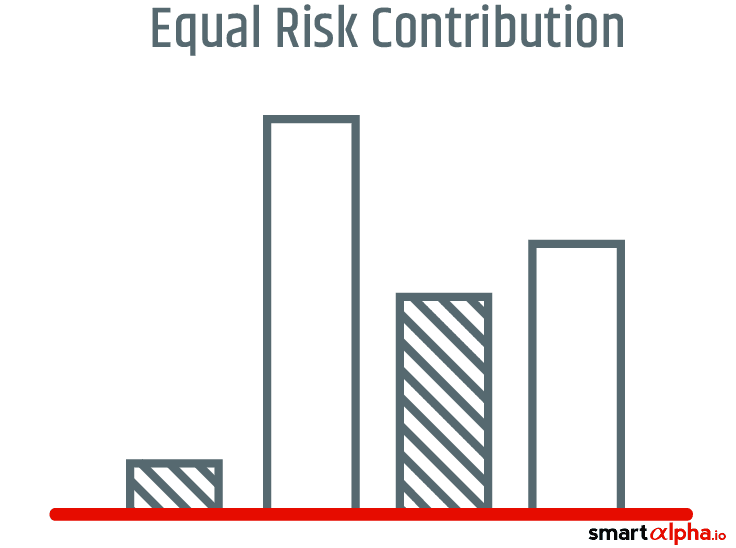

Managing a portfolio of Risk Premia indices requires accurate tools and analytics to help investors define the exact weighting scheme suited to their needs. For

There are a number of BRIC (Brazil, Russia, India, and China) indices available to investors. These economies are expected to show above-average growth.

With the market for smart beta and risk premia products maturing, emphasis is shifting from the selection of individual strategies towards building portfolios.